New Mileage Rate...With a Twist

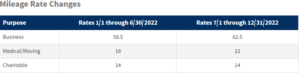

The IRS recently announced that, beginning July 1st, the mileage rates for business travel, as well as deductible medical/moving travel has increased 4 cents to $0.625 and $0.22 per mile respectively. (Charitable miles remains the same at $0.14 per mile) The "twist" to this is the mileage recorded for the first 6 months of the year will be $0.585 ($0.18 medical/moving) per mile, and the second 6 months will be $0.625 ($0.22 medical/moving) per mile.Make certain you are dating your mileage log, and updating your mileage tracking apps, to reduce the confusion and headache at the end of the year!

2022 Required Minimum Distributions (RMD’s) & Life Expectancy Table

There is a major change in RMD’s for tax year 2022; most notably the new Life Expectancy Table. For individuals receiving RMD’s, your minimum distribution will change, and it will be a smaller percentage. Congress is realizing that Americans are living longer (even with COVID?), and therefore need to make certain we have ample retirement (but not from Social Security) to live on. Please discuss this with your Financial Planning professional.

In addition to updated life expectancy tables, they have also raised the age to begin taking RMD’s to age 72, instead of 70 ½ like was the case before 2020. If you reach 72 in 2021, you must take your RMD by April 1st of the year after you turn 72. In general, the year after you turn 72, you could be required to take two RMD’s (one by April 1st of that year, and a second one by December 31st of the same year to apply towards the following year); then take the normal by the December 31st deadline each year after that. If you don’t want to pay tax for both in the same year, you are permitted to take a distribution the year of your 72nd birthday instead of waiting until April of the following year.

Feel free to use this link from the IRS to see the new life expectancy table and a simple calculator to determine your current and future distribution amounts.

(Remember, if you are the beneficiary of an IRA, this rule applies to you, but using the age of the deceased beneficiate, and our age is younger.)

Virtual Currency

As much as we wanted to bury our heads in the sand and act like this trend was a flash in the pan, we have realized it is here to stay. So has the IRS, and they are catching on quickly! Both Ryan and Don have taken classes on this topic so we can keep up with our clients and their tax responsibilities. If you have questions, or more importantly, if you hold any cryptocurrency, please make us aware of this during discussions with us and when delivering/sending in your information. You will need to report all transactions. We will ask you for them.

Tax Law Changes for 2020

2020 has been a one-of-a-kind year. Everyone has been affected in some way or another. No matter how this year ends, or if he just morphs into next year, there are only two things in life you can count on…death and taxes. So as “generous” as the government has been (or hasn’t been) this past year, their “payday” is right around the corner. It’s not all bad, though; most of the tax law changes are still aimed at easing the economic impact of the pandemic as well as expanding opportunities for increasing retirement savings.

Below are the most prominent to date. Check back with us at Lewis Financial Tax Service, LLC for other changes specific to you and any additions that will undoubtedly come with a new President.

(Disclaimer: The following is a list of items that have changed the tax law due to the passing of the SECURE Act, CARES Act, and others. Once the Presidency changes hands in January, there will likely be other tax law updates.)

2020 Recovery Rebates

Also known as the “stimulus checks”, it was more specifically a rebate for 2020 that was paid early. Receiving any amount of payment will not reduce your refund for the 2020 tax year. However, if you didn’t qualify for the rebate, or only received a partial “phase out” amount, that amount could be increased if your income was different in 2020 as opposed to 2019 OR there was an added dependent.

Charitable contributions

Nonitemizers can claim up to $300 in charitable cash donations. For itemizers, the limitation of 60% of your modified income has been pushed to 100% for cash contributions. It remains at 50% for non-cash items

Educators

Teachers who don’t itemize, can claim $250 in educator expenses this year. If two educators are married and filing jointly, that number is $500. (These expenses must be unreimbursed.)

Self-Employed Family and Medical Leave

Self-employed individuals can receive a credit against the Self Employment Tax. This applies if you were forced to quarantine based on federal, state, or local order, or medical advice; or if you were caring for someone who met those conditions; or caring for a son or daughter whose daycare had been closed due to Covid-19 precautions. The amount varies so much that it would be best to just contact us so we could discuss it.

Employers Paid Family and Medical Leave

This is too in-depth to begin to discuss here. However, we are up to speed with every aspect of the Families First Coronavirus Response Act, so please contact Ryan for a FREE consultation.

Required Minimum Distributions (RMDs)

The RMD rules have been waived for certain plans and IRAs for 2020. The required beginning date for RMDs has changed from 70 ½ to 72 for individuals turning 70 ½ after 2019.

Retirement Early Distributions

The 10% early withdrawal penalty has been waived for distributions up to $100,000 from IRAs and 401(k) plans. These distributions must be made between January 1, 2020 and December 31, 2020.You can elect to have the income from these distributions taxed over a three-year period, and you may also elect to recontribute the funds to an eligible plan within three years without regard for that year’s cap on contributions. Please note: the CARES Act provision must be included in your plan.

Traditional IRA Contributions

The maximum age limit of 70 ½ has been repealed.

New Standard Deduction (Update for inflation)

While only 13.7% of Americans now itemize following the JCJA in 2018, the IRS continues to increase the Standard Deduction each year for inflation. (Reminder: You don’t have to itemize to claim the $300 charitable contribution discussed above) Tax Year 2020 table:

Single: $12,400 (+$200); $14,050 if over age 65

Married Filing Joint: $24,800 (+$400); additional $1,300 each individual over age 65

Head-of-Household: $18,650 (+$300); additional $1,650 each individual over age 65

Standards Mileage Rates

Business: $0.575 per mile

Medical & Military Relocation: $0.17 per mile

Charitable: $0.14

Others

There are many more tax tables that have changed that are more specific to certain clients and would be too in-depth for the purpose of this entry. Please reach out to us regarding any other tax tables that may apply to you. Contact US.

What Does the Tax Cuts and Jobs Act (TCJA) Mean For Landlords?

In 2018, the TCJA was passed with mixed reviews. It benefited some, while others thought it would cause their refund to shrink. (For the most part, it didn’t) Here we will lay out some of the perks that Landlords received because of the TCJA.

The biggest news for small business owners was the 20% pass‐through deduction. This applied to a vast majority of individuals who ran their rental business as a sole proprietor, limited liability companies (LLCs), or partnerships. With these entities, any profit earned from rental activity is “passed through”. If your rental activity qualifies as a business for tax purposes (see below), rental owners may be eligible to deduct an amount equal to 20% of their net rental income. This is in addition to other rental‐related deductions. Put another way, they will effectively be taxed on 80% of their net rental income.

“WHO” QUALIFIES?

To receive the 20% tax deduction, you must meet both of the following qualifications:

- You operate your rental business as a sole proprietor, LLC owner, partner in a partnership or S‐corporation shareholder, and

- your total taxable income from all sources, after deductions, is $163,300 (filing single) or $326,600 (married filing jointly).

- You do not need to itemize to receive this deduction. If a taxpayer is above the income threshold, the amount of the deduction begins phasing out at these amounts and the deduction will be ZERO once the income reaches $213,300 (single) or $426,600 (married filing jointly). If a taxpayer exceeds the maximum threshold, you may still be able to claim the 20% deduction, However, your deduction cannot exceed:

- 50% of the W‐2 wages paid by the business

OR

- 25% of the W‐2 wages paid by the business plus 2.5% of the unadjusted basis of the business’ qualified property.

“WHAT” QUALIFIES?

As stated above, to receive this deduction, your rental activity must “qualify as a business for tax purposes”. For any activity to be a business, an individual must “engage in it regularly and continuously, primarily to earn a profit”. However, the IRS has created a “safe harbor” rule for this pass‐through deduction. Under this “safe harbor”, a rental activity is deemed a business if it meets the following standards:

- Keep separate books for each rental real estate you own,

- perform 250 hours of real estate rental services each year, and ∙ document what rental real estate activities are performed (a journal).

ANYTHING ELSE?

In the past, rental property owners were unable to deduct the cost of personal property used in residential units. Landlords scored a major victory when that was repealed in the TCJA. Landlords can now use bonus depreciation to fully deduct the cost of personal property all in the first year put into service. Personal property items include appliances, laundry equipment, gardening equipment and furniture.

Listed property must be used over 50% of the time for business to qualify for bonus depreciation. Listed property includes cars, TV’s and other entertainment property. Computers used to be on this list but are no longer. Therefore, you do not need to use a computer 50% of the time for business to qualify it for bonus depreciation. But if used less than 100% for business, the bonus percentage will also decline.